Bitcoin Macroeconomic Model and Its Potential as a Macro Asset

10 February, 2025

Bitcoin has evolved from an experimental peer-to-peer digital currency into a globally recognized financial asset with increasing macroeconomic significance. As institutional adoption grows and economic conditions shift, Bitcoin is being evaluated alongside traditional macro assets—such as gold, sovereign bonds, and reserve currencies. This article employs a rigorous macroeconomic framework grounded in the Quantity Theory of Money (QTM) to analyze Bitcoin’s potential as a leading macro asset. By examining its supply constraints, velocity trends, and macroeconomic interactions, I provide insights that are both empirically grounded and actionable for investors and policymakers.

Bitcoin and the Quantity Theory of Money

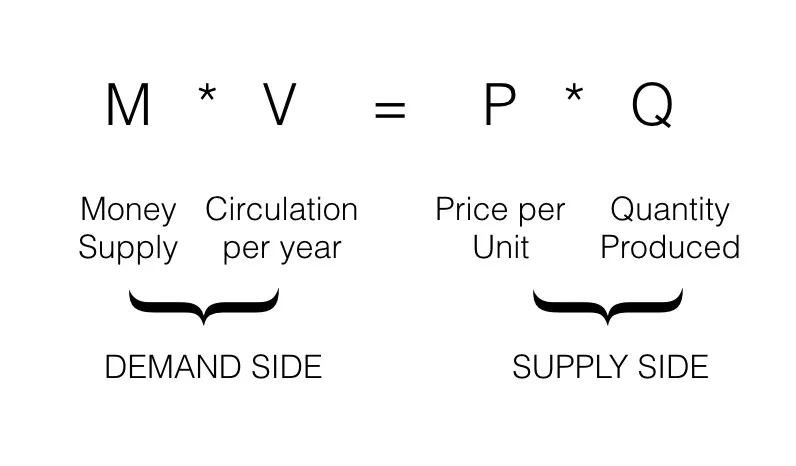

The classical Quantity Theory of Money is given by the equation:

MV = PQ

where M is the money supply, V is the velocity of money, P is the price level, and Q represents real expenditures. To adapt this framework for Bitcoin, we express all quantities in fiat currency units (thus setting Q = 1), which allows us to interpret P as the fiat value of Bitcoin.

Bitcoin’s money supply is defined by the product of the number of Bitcoin in circulation (B) and the price per Bitcoin (P). That is:

M = B * P

Given that B is algorithmically fixed and changes slowly over time, the primary determinant of P becomes Bitcoin’s velocity, V, which we decompose based on Bitcoin’s use. Specifically, we assume each Bitcoin is either saved or transacted, with the likelihood of being transacted given by τ (and, by definition, the likelihood of being saved equal to 1 - τ). Under the assumption that saved Bitcoin does not contribute to transactional velocity and that the velocity of transacted Bitcoin is approximately a linear function of transactional volume (scaled by a constant k), we can express the overall velocity as:

V = k * τ

Substituting these relationships back into our modified QTM yields:

P = (k * τ) / B

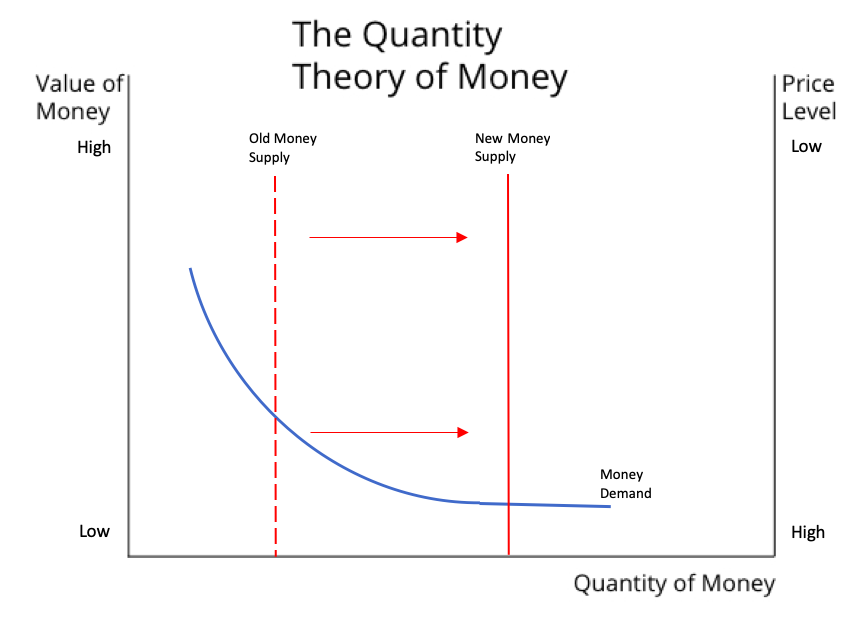

This formulation implies that Bitcoin’s price is primarily driven by the probability that a Bitcoin is saved rather than transacted. Empirical examples, such as the price surges during the Cyprus banking crisis and the rise of Chinese Bitcoin exchanges in 2013, support this view: external shocks that increase the propensity to save Bitcoin have historically driven its price higher, while routine transactional activity has a muted effect.

Empirical Data and Implications of Our Model

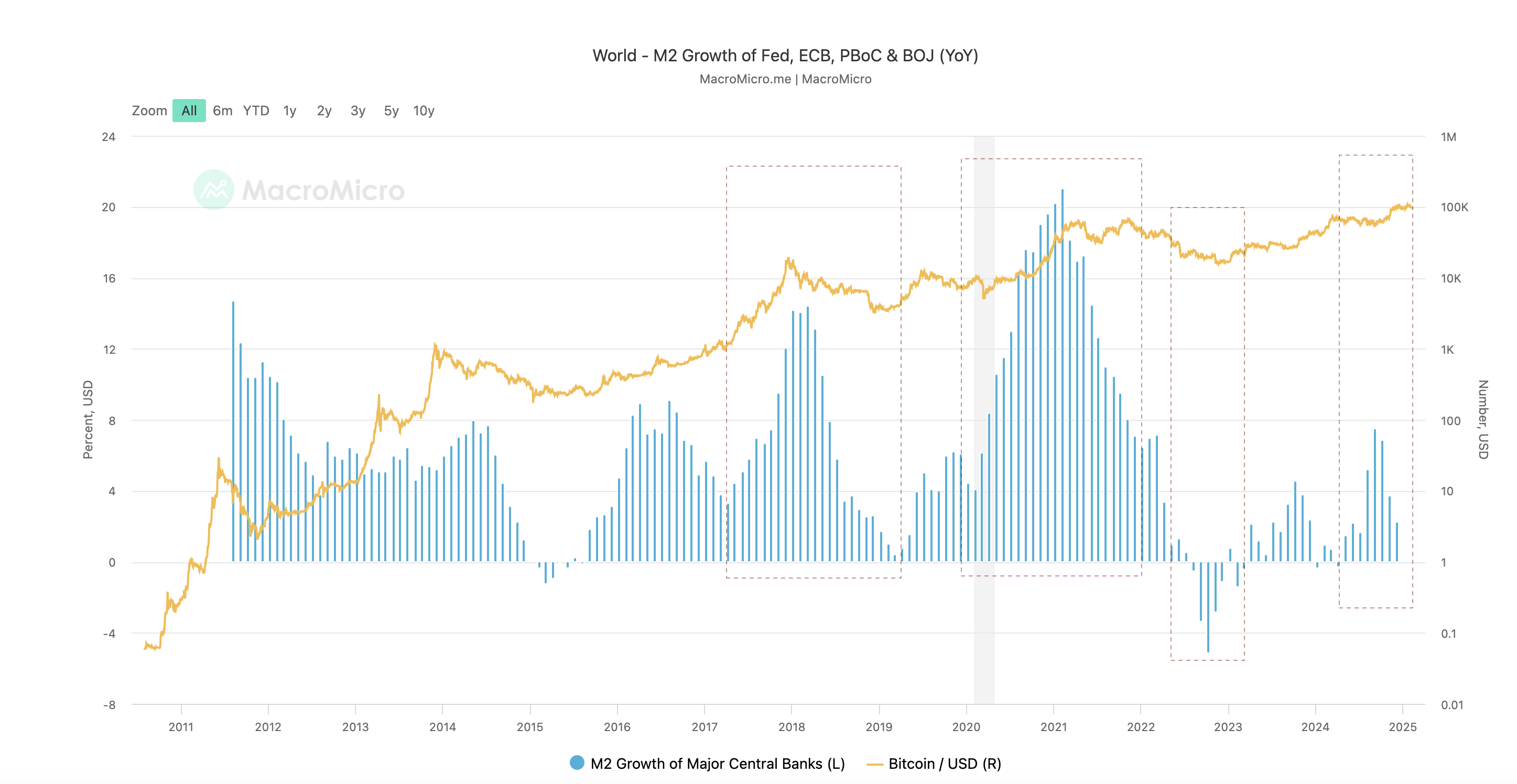

On-chain data and exchange turnover rates indicate that Bitcoin’s velocity has declined over the long term, particularly as institutional investors enter the market. Historical data suggests a strong relationship between global M2 expansion and Bitcoin’s price movements, with correlations at times exceeding 0.9 during periods of aggressive monetary stimulus. While forecasting future M2 growth remains uncertain, the unprecedented surge during the pandemic implies that further expansion on a similar scale may require another major economic shock—a true "black swan" event. In such scenarios, traditional asset correlations can shift unpredictably, with investor focus turning to liquidity, availability, and perceived safe-haven characteristics. Bitcoin, with its fixed supply and increasing institutional adoption, has the potential to benefit, though its behavior in crisis periods has varied. Key macroeconomic variables suggest that if central banks continue to expand balance sheets amid low real interest rates, Bitcoin’s role as a store of value—and therefore its macro asset characteristics—could be further reinforced.

Our model suggests that Bitcoin’s price dynamics are highly sensitive to macroeconomic conditions. As investors increasingly view Bitcoin as a hedge against fiat debasement, its store-of-value function strengthens. Conversely, if Bitcoin’s velocity were to rise sharply due to widespread transactional adoption, its price stability could be affected, making it behave more like a medium of exchange rather than a macro asset.

Challenges and Future Outlook

Despite Bitcoin’s growing macroeconomic relevance, several challenges remain:

- Volatility and Market Maturity – While increased institutional adoption has contributed to greater liquidity, Bitcoin’s volatility remains a barrier to broader portfolio integration. However, historical trends indicate that as Bitcoin's market capitalization grows, its volatility tends to decrease.

- Regulatory Uncertainty – Bitcoin operates in a fragmented regulatory landscape. Clarity in legal frameworks could provide stability, encouraging institutional adoption. The case of ETFs and structured financial products integrating Bitcoin illustrates the potential impact of regulatory approval on market confidence.

- Macroeconomic Correlations – Bitcoin’s correlation with traditional risk assets, such as equities, fluctuates over time. While it is often seen as a hedge against inflation and monetary debasement, its behavior in market downturns remains complex and requires further study.

Conclusion

This article presents a quantitative framework for analyzing Bitcoin as a macro asset using the Quantity Theory of Money. By modifying the traditional QTM to account for Bitcoin’s fixed supply and the interplay between savings and transactions, we observe that Bitcoin’s price is primarily influenced by investor sentiment regarding its store-of-value function. Empirical evidence highlights that macroeconomic factors—such as monetary policy shifts and liquidity conditions—play a pivotal role in shaping Bitcoin’s valuation.

Key takeaways for practitioners include:

- Monitoring on-chain data to gauge shifts in Bitcoin’s transactional versus savings behavior.

- Tracking macroeconomic indicators, such as real interest rates and central bank policies, as key drivers of Bitcoin’s price movements.

- Assessing Bitcoin’s integration into institutional portfolios, considering its evolving role relative to traditional safe-haven assets.

Future research should refine econometric models by incorporating real-time transaction data and alternative macroeconomic variables. As Bitcoin’s adoption progresses, its characteristics as a macro asset will continue to evolve, making ongoing quantitative analysis essential for investors and policymakers alike.